Study Material & Notes-Partnership – Admission of Partner

Study Material & Notes for the Chapter 5

Partnership - Admission of a Partner

I. ADMISSION – MEANING, NEED AND EFFECTS

A. Meaning of Admission of a Partner

An existing partnership firm may take up expansion/ diversification of the business. In that case it may need managerial help or additional capital. An option before the partnership firm is to admit partner/partners. When a person is admitted to the existing partnership firm, it is called admission of a partner.

B. Partners Consent

According to the Partnership Act 1932, a person can be admitted into partnership firm only with the consent of all the existing partners unless otherwise agreed upon.

C. Firm Reconstituted

On admission of a new partner, the old partnership comes to an end and the partnership firm is reconstituted with a new agreement. However the partnership firm continues

Reconstitution of a firm always leads to change in the existing profit sharing ratio

D. Rights of a new Partner

Right to share profits in future

Right to share assets of the firm

II. DETERMINATION OF NEW PROFIT-SHARING RATIO & SACRIFICING RATIO

A. Adjustment in Profit Sharing Ratio

The new profit-sharing ratio is decided mutually between the existing partners and the new partner. The incoming partner acquires his share of future profits either from one or more existing partner.

B. Sacrificing Ratio

C. Premium For Goodwill

New partner compensates the existing partners who sacrifice their share of profits in his/her favour.

The amount new partners pays against this sacrifice is known as Premium For Goodwill

D. Adjustments on Admission

Adjustment in profit sharing ratio;

Adjustment of Goodwill;

Adjustment for revaluation of assets and reassessment of liabilities;

Distribution of accumulated profits and reserves; and

Adjustment of partners’ capitals.

E. Sacrificing/(Gaining) Share

Sacrificing/(Gaining) Share = Old Share – New Share

If a Partner’s Old Share – New Share is Positive (+) figure then the partner has made a sacrifice

If a Partner’s Old Share – New Share is Negative (-) figure then the partner has made a gain

Case-1 New partner share from old partners is already given - From Case

In this case, the new profit sharing ratio of the existing partners is to be ascertained after deducting the sacrifice of share agreed from his share. It means the incoming partner has purchased some share of profit in a particular ratio from the existing partners.

Sacrificing ratio is share surrendered

Case-2 New partner gets his share from existing partners in a particular ratio – OF Case

In this case, the new profit sharing ratio of the existing partners is to be ascertained after deducting the sacrifice of share agreed from his share. It means the incoming partner has purchased some share of profit in a particular ratio from the existing partners.

Sacrificing ratio is share surrendered

Case-3 Only new partner share as a portion of firm’s profits is given- Certain Case

In this case, it is presumed that the existing partners continue to share the remaining profit in the same ratio in which they were sharing before the admission of the new partner. Then, existing partner’s new ratio is calculated by dividing remaining share of the profit in their existing ratio. Sacrificing ratio is calculated by deducting new ratio from the existing ratio.

Sacrificing ratio is old partners existing ratio

III. PREMIUM FOR GOODWILL

A. Why Premium for Goodwill

Accumulated Losses include

The new partner acquires his/her share of profit from the existing partners. This will result in the reduction of the share of existing partners. Therefore, the existing partners asks for Compensation for sacrifice of their profits, he/she compensates the existing partners for the sacrifices this compensation is called Premium for Goodwill. He/she compensates them by making payment in cash or in kind. The payment is equal to his/her share in the goodwill.

B. Premium for Goodwill

Premium for Goodwill = Goodwill of the Firm X New Partner’s Share

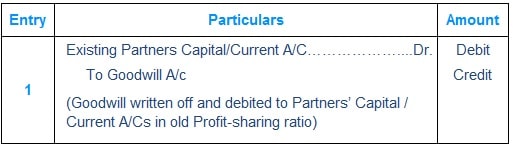

If Goodwill is already appearing in the books

As per Accounting Standard-26 (AS-26), goodwill can be recorded/debited in the books only when some consideration in money or money’s worth has been paid for it. Thus only purchased goodwill should be recorded in the firm’s books

If at the time of admission of a new partner, goodwill is appearing in the Balance sheet of a firm, it would be desirable to close the Goodwill Account

Journal Entries

C. Premium for Goodwill – Various Scenarios

All good firms take necessary safety precautions and train their workmen to avoid any accidents

At the factories/workplace despite all safety precautions and training there may be a situation wherein a worker might meet an accident resulting into medical treatment or disability.

Since the accident taken place at the Firm’s premises, there is a claim from the workmen/employee

To meet such contingencies, good firms generally set aside funds and create specific reserve Workmen Compensation Reserve

Any claim from workmen is paid out of the Workmen Compensation Reserve

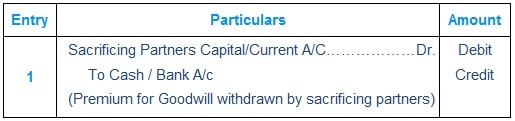

If Premium For Goodwill withdrawn by the existing partners

Journal Entries

Important to Note: The Assets and Liabilities remain at the book value. No adjustment in the Balance Sheet of the revalued assets/liabilities

D. Hidden Goodwill

Firm’s Goodwill = Total Capital – Net Worth

Where:

Total Capital = New Partner’s Capital X Reciprocal of New Partner’s share

Net Worth = Adjusted Existing Partners Capital + New Partner’s Capital

Computation of Net Worth (Liabilities Side Approach) = Existing Partner’s Capital + Free Reserves + Revaluation Profit – Revaluation Loss – Accumulated Losses – Existing Goodwill – Fictitious Assets

Computation of Net Worth (Assets Side Approach) = Total Assets – Outside Liabilities + Revaluation Profit – Revaluation Loss – Accumulated Losses – Existing Goodwill Fictitious Assets

Premium For Goodwill = Goodwill of the Firm X New Partner’ Share

IV. ACCOUNTING OF RESERVES, ACCUMULATED PROFITS/LOSSES

On admission of a new partner, the existing partners scans Firm’s Financial position (Balance Sheet) i.e. Reserves, Accumulated Losses, Assets & Liabilities

The logic behind this exercise is the new partner should not get undue benefit due to previously earned/unearned profits or suffer loss due to previous earned/unearned losses.

During this scanning process Partners may find Free Reserves like General Reserve, P&L (Cr), these are distributed among existing partners in their current profit-sharing ratio.

Specific purpose reserves like (a) Workmen Compensation Reserve are compared with any workmen claim (b) Investment Fluctuation Reserve is compared with market value of Investments and any excess reserve is distributed to existing partners in their current Profit-sharing ratio and any short reserve is taken to Revaluation A/c.

Partners may also find Undistributed Losses or Fictitious Assets, these are written off and charged to the existing Partners in their current Profit-sharing Ratio.

Partners reevaluate market value of Fixed Assets and remeasure Current Assets and Current Liabilities. Any change in the value of Assets/Liabilities is dealt via Revaluation Account and the resultant gain/loss is shared amongst the existing partners in their current profit-sharing ratio.

A. Accounting treatment of Accumulated Losses

Accumulated Losses include

Debit balance in Profit & Loss A/C

Deferred revenue Expenses

Preliminary Expenses

Advertisement Suspense A/C

Journal Entry for writing off Accumulated Losses

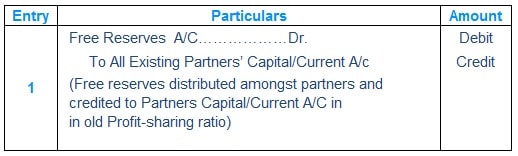

B. Accounting treatment of Free Reserves

Free Reserves include

Credit balance in Profit & Loss A/C

General Reserve

Accumulated Profits

Contingency Reserve

Journal Entry for distributed Reserves amongst partners

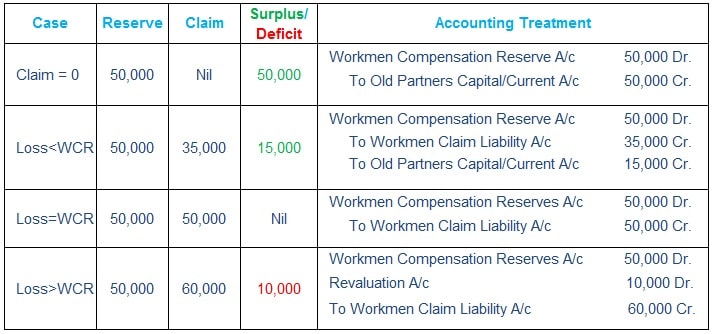

C. Workmen Compensation Reserve

All good firms take necessary safety precautions and train their workmen to avoid any accidents

At the factories/workplace despite all safety precautions and training there may be a situation wherein a worker might meet an accident resulting into medical treatment or disability.

Since the accident taken place at the Firm’s premises, there is a claim from the workmen/employee

To meet such contingencies, good firms generally set aside funds and create specific reserve Workmen Compensation Reserve

Any claim from workmen is paid out of the Workmen Compensation Reserve

Accounting Treatment under various scenarios

D. Investments Fluctuation Reserve

In case a firm has surplus funds, which are not be used in business immediately, invests these funds.

The Market value of the investments is not static and keeps on varying (higher/lower) due to various economic conditions

To protect from the risk of any loss due to fall in the value of investments, Good firms set aside reserve out of profits and create Investment Fluctuations Reserve

In case of a permanent fall in the value of Investments, Firm utilize Investment Fluctuation Reserve

Any excess Investment Fluctuation Reserve at the time of change in PSR is distributed amongst Partners’ in their old PSR

Accounting Treatment under various scenarios

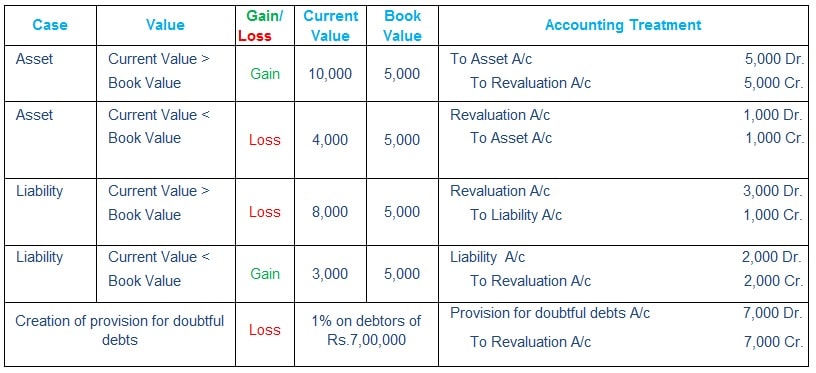

E. Revaluation of Assets/ Liabilities

Partners reevaluate market value of Fixed Assets and remeasure Current Assets and Current Liabilities. Any change in the value of Assets/Liabilities is dealt via Revaluation Account and the resultant gain/loss is shared amongst the existing partners in their current profit-sharing ratio.

Accounting Treatment under various scenarios

Important to Note:

Language in the question: AT/To means new value of the Asset/Liability.

Language in the question: By means difference between existing value and new value of the Asset/Liability.

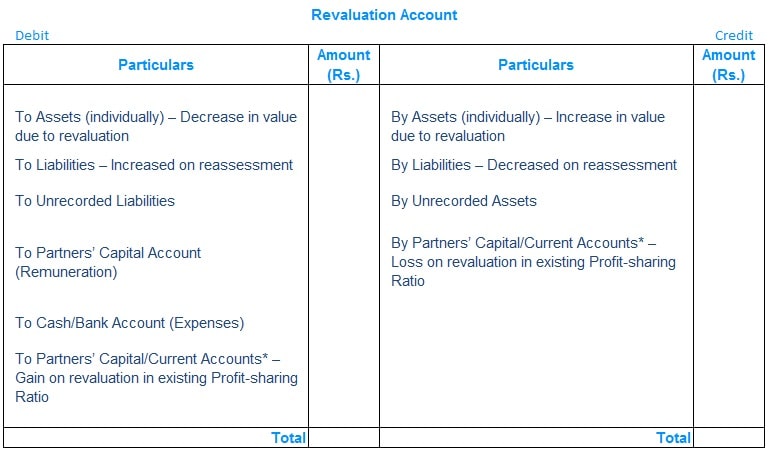

F. Preparation of Revaluation Account

On the Revaluation of Assets and Reassessment of Liabilities, a new account is opened Revaluation Account

Revaluation Account is a nominal account. As per nominal rule all the expenses & losses are debited and all the incomes/gains/profits are credited

V. ADJUSTMENT OF CAPITAL

Sometime, at the time of admission, the partners’ agree that their capitals be adjusted in proportion to their profit sharing ratio

Two methods of Adjustment of Capital

a) Capital of new partner’s is computed in proportion to the total capital of the new firm

b) Adjustment of existing partners capital on the basis of New Partner’s Capital

For this purpose, the capital accounts of the existing partners are prepared, making all adjustments, on account of goodwill, free reserves , accumulated losses and revaluation of assets/reassessment of liabilities.

The actual capital so adjusted will be compared with the amount of capital that should be kept in the business after the admission of the new partner.

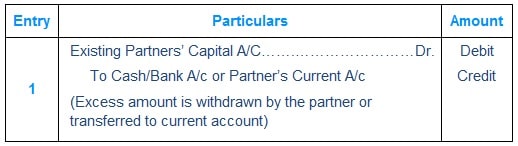

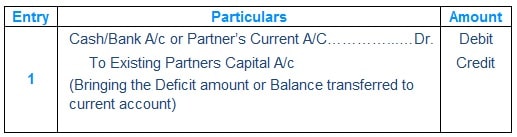

The excess if any, of adjusted actual capital over the proportionate capital will either be withdrawn or transferred to current account and vice versa.

When Revaluation Account is prepared, assets and Liabilities appear in the Balance Sheet of the reconstituted firm at their revised (changed) values

I. Capital of new partner’s is computed in proportion to the total capital of the new firm

The capital accounts of the existing partners are prepared, making all adjustments, on account of goodwill, free reserves , accumulated losses and revaluation of assets/reassessment of liabilities.

Compute Capital of new partner with reference to Combined Capital of existing partners

Step-1 Firm’s Total Capital = Combined adjusted closing capital of existing partners X Reciprocal of remaining share of existing Partners

Step-2 New Partner’s Capital = Firm’s Total Capital X New Partner’s share

II. Capital of new partner’s is computed in proportion to the total capital of the new firm

Step-1 Firm’s Total Capital = New Partner’s Capital X Reciprocal of new partner’s share

Step-2 Specific Partner’s New Capital = Firm’s Total Capital X Specific Partner’s share

Step-3 Specific Partner’s Existing Capital = Old Capital (+)(-) Adjustments of Goodwill, Reserves & Accumulated Losses

Step-4 Capital to be introduced/withdrawn = Specific Partner’s New Capital – Specific Partner’s Existing Capital

Journal Entries

a) When excess amount is withdrawn by the partner or transferred to current account.

b) For bringing in the Deficit amount or Balance transferred to current account.