Two types of Organizations – For Profit organization and Non-Profit Organization

A. For-Profit Organization

A For-profit organization is the one that operates with the mission is to generate profit and forward these profits to the business’s owners and shareholders as well as to maximize wealth of the owners/shareholders.

For-profit organizations can be in the form of a sole proprietorship, partnership firm or a company.

For-profit organizations develop effective products and services that are valuable to consumers and makes profit by directly/indirectly selling these goods or services.

For-profit organizations fund their assets through owner’s capital, loans and revenue generated from sales

Examples

Local kirana/groceries shop in your neighborhood (Sole proprietor)

A popular restaurant in your big market (Partnership firm)

Big Corporates – Reliance Industries, Tata Motors, Bata, Patanjali, Unilever, Indigo, Taj/Oberoi group of hotels, Airtel/Vodafone/Jio etc.

B. Non-Profit Organizations

NPO are organizations whose main objective is to render services to its members and society

These activities include charitable, religious, educational, scientific, literary, testing for public safety, fostering national or international amateur sports competition, and preventing cruelty to children, old or animals

Its profits/surplus is recycled back into the nonprofit corporation’s public benefit mission and activities.

A nonprofit organization can be constituted in the form of trust, clubs, society, committee

Nonprofits seek out private donations of time and money, corporate sponsorships, and government grants. They source revenue mainly through donations, subscriptions, or membership fees.

Examples

Red Cross Society, Earth Saviors Foundation, Child Rights and You

Gymkhana Club

Mata Chanan Devi Hospital

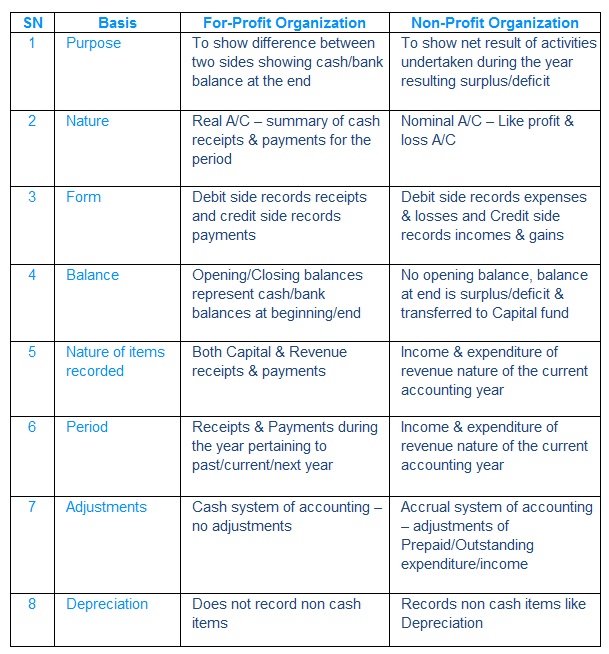

C. Difference between For-Profit & Non-Profit Organization

II. FUND BASED ACCOUNTING

NPO receives donations for specific purposes and accordingly create a specific fund for the said purpose

Two categories of fund – General Fund and Specific Fund

In the Fund based accounting, receipt of donations and incomes relating to a particular fund are credited to that fund and payments and expenses are debited to it

A. Funds – Inflow/Outflows

B. General Fund - Capital fund

C. Specific Fund – Building Fund

D. Intra Fund Adjustments

From building Fund to Capital Fund: Building Under Construction

Transfer from Building to Capital Fund (+) Capital Fund (-) Building Fund

E. Funds Fund expenses over Fund Balance (Specific Fund-Tournament Fund)

If after adding incomes to fund, further donations received and deducting expenses, the fund shows debit balance, it is transferred i.e., shown on the Debit side of Income and Expenditure A/c