A. Computation of Amount Due to the Retiring Partner

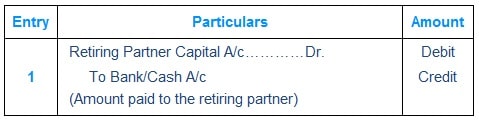

B. Settlement of Retiring Partner’s Claim – In Lumpsum

Retiring partners’ claim is paid either out of the funds available with the firm or out of funds brought in by the remaining partners.

Journal Entry

C. Settlement of Retiring Partner’s Claim – In Installments

Amount due to retiring partner is paid in instalments. Usually, some amount is paid immediately on retirement and the balance is transferred to his loan account.

This loan is paid in one or more instalments and the loan amount carries some interest.

In the absence of any agreement on interest rate, the retiring partner can claim interest @ 6% [as per Section 37 of the Indian Partnership Act 1932]

Installment has two parts – Principal Amount of Loan and Interest at agreed rates

Interest due on loan amount is credited to retiring partners’ loan account.

Instalment inclusive of interest then is paid to the retiring partner as per schedule agreed upon.

Journal Entry

D. Mid Term Retirement

Mid term retirement categorize the adjustments in two parts

From previous balance sheet date

Examples: Goodwill, Reserves, Undistributed Profits/Losses Misc. Expenditure on Assets side, revaluation Profit/Loss etc.

There is no change in these values if partner retires mid term

Period specific adjustments

Examples: like Salary, Drawings, Interest on Capital, Interest on Drawings, share of current account year profit/loss.

In such adjustments, time factor is used.

The Estimated Profit/Loss till the date of retirement is credited/debited to the Retiring partner A/c

Mid Term Retirement-Interest payment to Retiring Partner

Interest is accrued on (i) End of the Financial year and (ii) Date of Payment

Installment is paid on date of payment along with interest