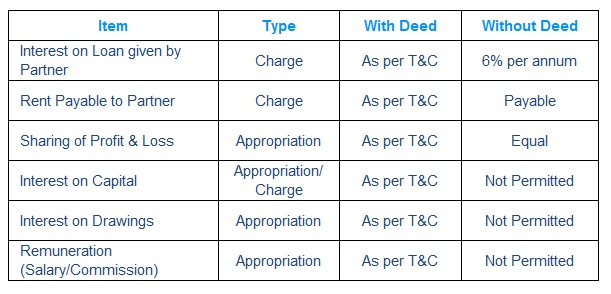

Partnership Fundamentals Notes1 Study Material & Notes for the Chapter 1 Partnership - Fundamentals I. PARTNERSHIP BASICS A. Partnership-Definition The Indian Partnership Act 1932, Section 4 “Partnership is the relation between persons who have agreed to share the profits of a business carried on by all or any of them acting for all.” Relation between personsWho have agreed (written/oral)To share the profits (losses)…business with a motive to earn profitsOf a business…legal business (theft/cheating, scam)Carried on by all orAny of them acting for all B. Nature of Partnership C. Nature of Partnership To share profits in an agreed ratioTo take part in the conduct of the businessRight to be consultedRight to inspect the books of accountsRight to retire from the firmTo disallow admission of new partners (Imp). Example 40 partners, want to admit new partner, one partner says No D. Contents of Partnership Deed Partnership agreement is the mutual understanding on which Partners decide to do a legal business to earn profits.It may be oral or written.The written, signed and registered version of the agreement is also called partnership deedDeed is optional/non mandatory/non compulsory but recommendedProfit will be distributed/apportioned as per the agreementAgreement once made needs to be honoured in all the conditionsThe Partnership Deed may contains basically two types of matters: Management related matters Money related matters E. Provisions relevant for Accounting F. Interest on Loan given by Partner Is a charge against profit (accrued even if no Profits)Interest rate is as provided in the Partnership deedIf no partnership deed or not provided in partnership deed – @6% p.a.Interest = Amount of Loan X Rate of Interest X TimeInterest is credited to Partner Loan Account (and not to Partner Capital/Current A/C) Journal Entry G. Rent Payable to Partner Is a charge against profit (accrued even if no Profits)Charge since rent is paid for using property for business purposeRent is credited to Rent Payable Account (and not to Partner Capital/Current A/C) Capital/Current A/C) Journal Entry H. Remuneration to Partner – Salary/Commission Payable only if provided in the partnership deedIf loss – it is not payable, If sufficient profits – Fully allowedIf insufficient profits – Profits are distributed in the ratio of Salary/Commission to be allowed Salary/Commission is credited to Partner’s Capital/Current Account Journal Entry