Revaluation Account

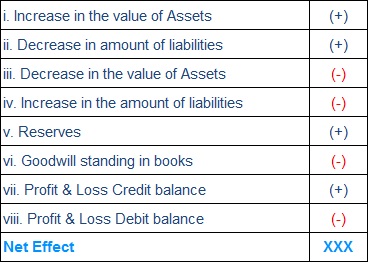

a) Calculation of the Net Effect of Revaluation

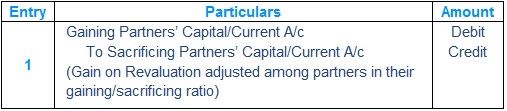

Journal Entry – In case of Gain/Profit on Revaluation

Journal Entry – In case of Loss on Revaluation

Revaluation Account

a) Calculation of the Net Effect of Revaluation

Journal Entry – In case of Gain/Profit on Revaluation

Journal Entry – In case of Loss on Revaluation