III. ACCOUNTING OF RESERVES, ACCUMULATED PROFITS / LOSSES

On reconstitution of partnership Firm, the partners scans Firm’s Financial position (Balance Sheet) i.e. Reserves, Accumulated Losses, Assets & Liabilities

The logic behind this exercise is the new relationship should not get undue benefit due to previously earned/unearned profits or suffer loss due to previous earned/unearned losses.

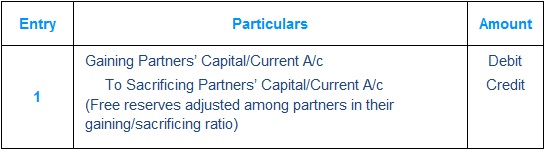

During this scanning process Partners may find Free Reserves like General Reserve, P&L (Cr), these are distributed among partners in their existing profit-sharing ratio.

Specific purpose reserves like (a) Workmen Compensation Reserve are compared with any workmen claim (b) Investment Fluctuation Reserve is compared with market value of Investments and any excess reserve is distributed to existing partners in their current PSR and any short reserve is taken to Revaluation A/c.

Partners may also find Undistributed Losses or Fictitious Assets, these are written off and charged to the existing Partners in their current Profit Sharing Ratio.

Partners reevaluate market value of Fixed Assets and remeasure Current Assets and Current Liabilities. Any change in the value of Assets/Liabilities is dealt via Revaluation Account and the resultant gain/loss is shared amongst the existing partners in their current profit-sharing ratio.

A. Accounting treatment of Accumulated Losses

Accumulated Losses include

Debit balance in Profit & Loss A/C

Deferred revenue Expenses

Preliminary Expenses

Advertisement Suspense A/C

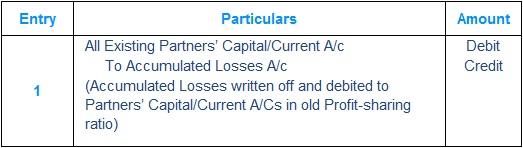

Method-1 Accumulated Losses are written off

Important to Note: If question is silent, Method-1 is the preferred treatment

Method-2 Accumulated Losses are carried forward

B. Accounting treatment of Free Reserves

Free Reserves include

Credit balance in Profit & Loss A/C

General Reserve

Accumulated Profits

Contingency Reserve

Method-1 Reserves are distributed amongst partners

Important to Note: If question is silent, Method-1 is the preferred treatment

Method-2 Accumulated Losses are carried forward

C. Workmen Compensation Reserve

All good firms take necessary safety precautions and train their workmen to avoid any accidents

At the factories/workplace despite all safety precautions and training there may be a situation wherein a worker might meet an accident resulting into medical treatment or disability.

Since the accident taken place at the Firm’s premises, there is a claim from the workmen/employee

To meet such contingencies, good firms generally set aside funds and create specific reserve Workmen Compensation Reserve

Any claim from workmen is paid out of the Workmen Compensation Reserve

Accounting Treatment under various scenarios

D. Investments Fluctuation Reserve

In case a firm has surplus funds, which are not be used in business immediately, invests these funds.

The Market value of the investments is not static and keeps on varying (higher/lower) due to various economic conditions

To protect from the risk of any loss due to fall in the value of investments, Good firms set aside reserve out of profits and create Investment Fluctuations Reserve

In case of a permanent fall in the value of Investments, Firm utilize Investment Fluctuation Reserve

Any excess Investment Fluctuation Reserve at the time of change in PSR is distributed amongst Partners’ in their old PSR