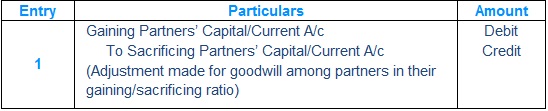

If Partners decide to change their profit-sharing ratio, the gaining partner must compensate the sacrificing partner

The compensation by gaining partner to the sacrificing partner is payment of Goodwill in the gaining ratio

If Partner B gained 1/10 of the share and Partner A scarified 1/10 of the share and goodwill of the Firm is Rs. 5,00,000/- then Partner B should compensate Partner A for: Rs. 5,00,000 X (1/10)= Rs. 50,000/-

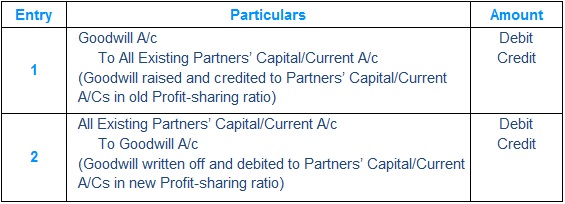

Case-1 Goodwill is not appearing in the books of accounts

Method-1 Goodwill is raised and then written off

Method-2 Goodwill is adjusted through Partners’ Capital Accounts

Important to Note: If question is silent, treat Capital Accounts as Fluctuating

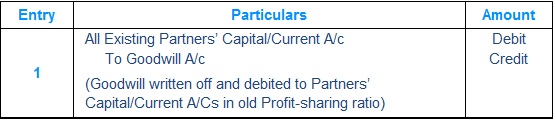

Case-2 Goodwill is appearing in the books of accounts

Method-1 Existing Goodwill is written off

Important to Note: If question is silent, Method-1 is the preferred treatment

Method-2 Effect is given to the net increase or decrease in goodwill