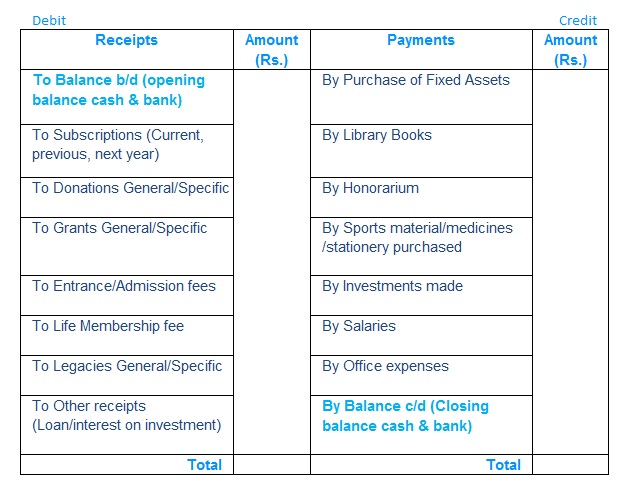

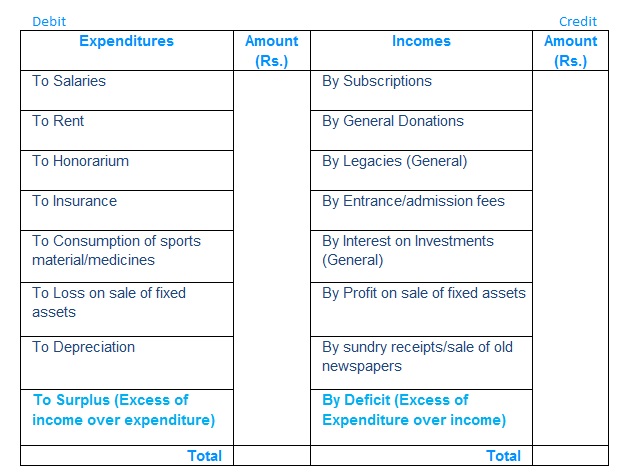

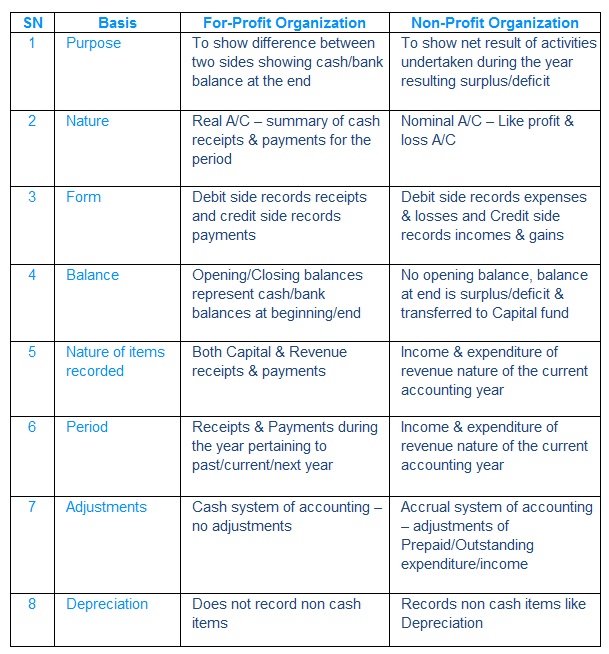

NPO Notes5 Study Material & Notes for the Chapter 1 Non-Profit Organization V. FINANCIAL STATEMENTS A. For-Profit Organization & Non-Profit Organization B. Capital & Revenue Receipts C. Capital & Revenue Payments D. Receipts and Payments Account Like Cash AccountOnly Cash transactions are recorded, credit/accrual transactions are not recordedIs a summary of cash and bank transactions prepared at the end of the accounting year Receipts include Capital as well Revenue Receipts, similarly Payments include both Capital & Revenue PaymentsReceipts & Payment could pertain to any Accounting year…Current, previous, or future Receipts & Payments Account E. Income & Expenditure Account Like Profit & Loss Account…summary of Income & Expenditure of an accounting yearTransactions are recorded on accrual basis hence both cash & credit transactions are recordedOnly transaction of revenue nature is recorded, capital transactions are not recorded Accrual adjustments done (+)/(-) Outstanding at end/beginning (+)/(-) Prepaid at the beginning/endIf Income > Expenditure, it is surplus else Deficit (Expenditure > Income) Receipts & Payments Account F. Difference between Receipts & Payments Account and Income and Expenditure Account G. Balance Sheet Balance Sheet shows the Financial position of an NPO at the reporting date/end of accounting yearSimilar to Balance sheet of For Profit OrganizationsThe Balance sheet shows Capital Fund, Specific fund, Liabilities and AssetsSurplus/deficit of the Income & Expenditure Account is shown under Capital fundIf Opening Capital Fund is not given, it is computed making Opening Balance Sheet Balance Sheet