When a company issues debentures, it has to pay interest thereon at fixed percentage periodically (quarterly/half yearly/yearly) until debentures are repaid

Interest is computed at the nominal value of debentures.

This percentage is usually as part of the name of debentures like 8% debentures, 10% debentures, etc.

Interest on debenture is a charge against the profit of the company and must be paid regularly even when Company suffers a loss or does not earn profits.

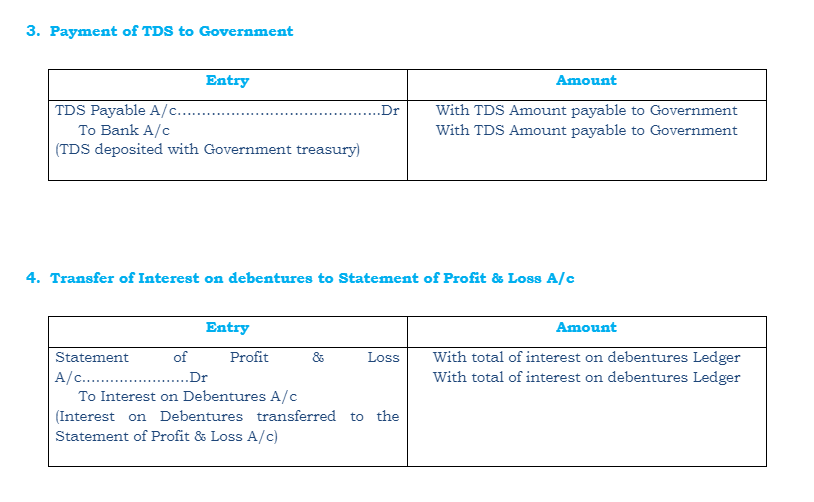

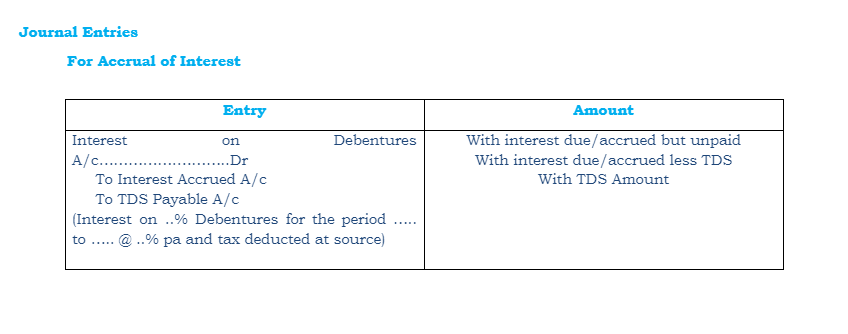

According to Income Tax Act, 1961, a company paying interest on debentures is required to deduct income tax at the prescribed rate from the gross amount of debenture interest (if it exceeds the prescribed limit) before any payment is made to the debenture holders (Tax Deducted at Source).

Illustration

Debenture Face Value

Rs. 100

Number of Debentures

10,000

Period

6 months

Interest rate

9% per annum

Profit & Loss A/c

Loss Rs. 75,00,000

Interest Amount

(10,000×100)x9%x6/12 = Rs. 45,000

Income Tax (TDS) @ 10%

45,000×10% = Rs. 4,500/-

Interest Net of TDS

45,000-4,500=Rs. 40,500

Interest on Debentures - Accrual

Interest may be paid periodically and the period may be quarterly, half-yearly or yearly

The date of payment of interest may be coincide with the end of the accounting period

For example interest is payable half yearly on 30th Jun and 31st December

In this case, at the end of the accounting year on 31st March, interest for the period 1st Jan to 31st Mar needs to be accrued in the books of accounts