A collateral security may be defined as a subsidiary or secondary or additional security besides the primary security

Whenever a company takes loan from bank or any financial institution it may issue its debentures as secondary security

Such an issue of debentures is known as ‘Issue of Debentures as Collateral Security’

No interest is paid on the debentures issued as collateral security because company pays interest on loan

The liability of the Company is towards the loan availed and not for the face value of debentures issued

If the company fails to repay the loan along with interest, the lender is free to receive his money from the sale of primary security and if the realisable value of the primary security falls short to cover the entire amount, the lender has the right to invoke the benefit of collateral security whereby debentures may either be presented for redemption or sold in the open market.

In case the need to exercise this right does not arise, debentures will be returned back to the company.

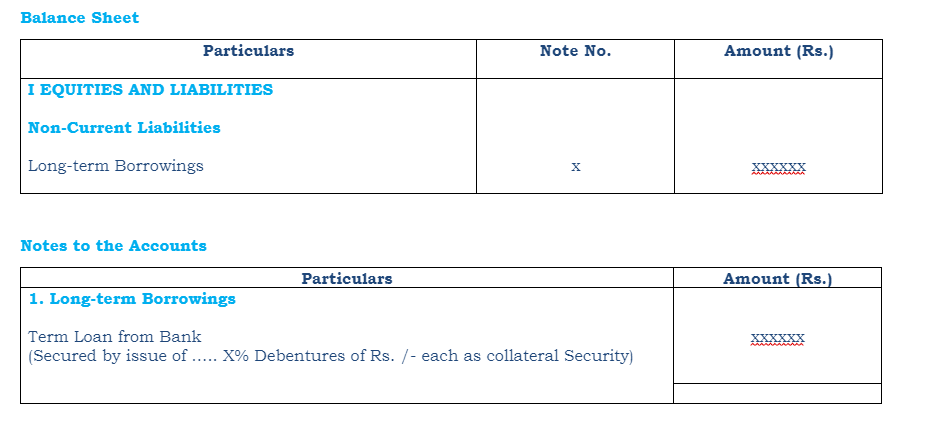

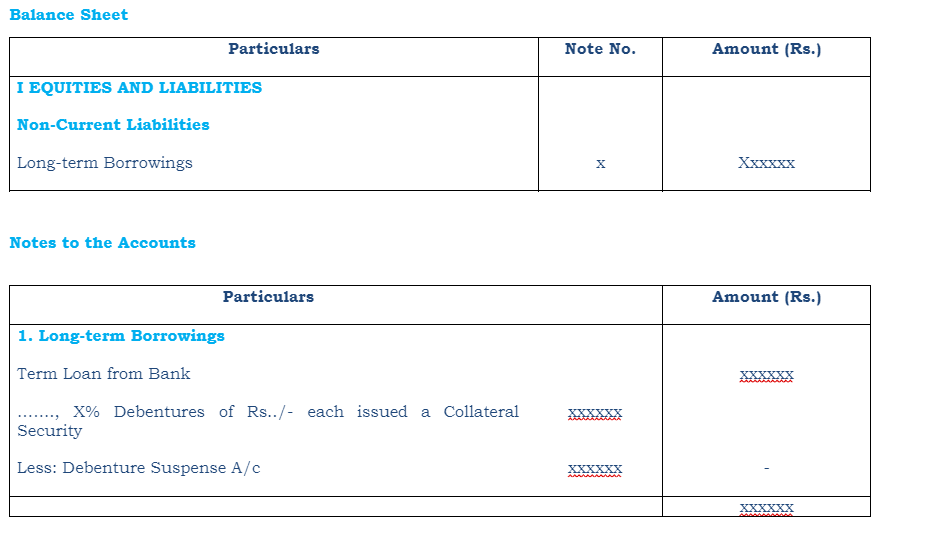

Accounting Treatment

Method-1 No Journal Entry is passed

No entry is made in the books of accounts since no liability is created by such issue.

However, on the liability side of the balance sheet, below the item of loan, a note to the effect that it has been secured by issue of debentures as a collateral security is appended.