II. ISSUE OF DEBENTURES FOR CONSIDERATION OTHER THAN CASH

A. On Purchase of Assets

Where a company has purchased assets from a vendor and enters into an arrangement with the said vendor that instead of settlement of his dues in cash, the vendor agrees to accept fully paid debentures of the company issued to them.

These debentures can be issued at par, at premium or discount and the number of debentures to be issued will depend upon the price at which the debentures are issued and the amount payable to the vendor

The number of debentures issued to the vendor will be calculated as = Amount Payable/Issue Price

B. On Purchase of Business

Where a company purchases business of another entity and enters into an arrangement with the said entity that instead of settlement of their dues in cash, the owners of the entity agrees to accept fully paid debentures of the company issued to them.

These debentures can be issued at par, at premium or at discount and the number of debentures to be issued will be calculated as Purchase Consideration Amount/Issue price

C. Issue of Debentures to Promoters

Sometimes debentures are issued to the promotors of the company in lieu of the services provided by them during the incorporation of the company.

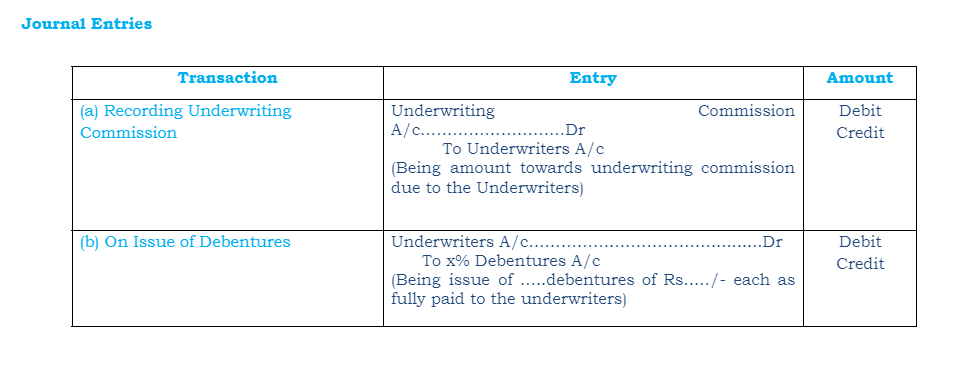

D. Issue of Shares to Underwriters

Underwriters undertake to subscribe the securities that remain unsubscribed by public. The Underwriter charges a commission for his servicers.