I. MEANING, FEATURES, TYPES AND ISSUE OF DEBENTURES

A. Definition

According to Section 2(20) of the Companies Act, 2013, “Debenture includes debenture stock, bonds or any other instrument of a company evidencing a debt, whether constituting a charge on the assets of the company or not”

a) Meaning

Debenture is a written instrument acknowledging a debt under the common seal of the company. It contains a contract for repayment of principal after a specified period or at intervals or at the option of the company and for payment of interest at a fixed rate payable usually either half-yearly or yearly on fixed dates.

b) Bond

Bond is also an instrument of acknowledgement of debt. In the Bond instead of rate of interest amount payable on maturity is mentioned.

c) Any other Instrument evidencing a debt

It means any instrument other than debenture or bond issued by the Company substantiating borrowing. For example Company invites money from Pubic in the form of Pubic deposits

d) Charge

According to Section 2(16) of the Companies Act, 2013, Charge is an interest or lien created on the assets or property of a Company or any of its undertaking as security and includes a mortgage

Charge on assets means the right of the lender to be paid from a borrower’s asset if the debt is not paid on time.

e) Debenture holders

The persons to whom the debentures are issued, are called debenture holders. The debenture holders are not the owners of the company. They are the lenders of the company.

f) Trust Deed

The Company issuing debentures to public is required to appoint trustees and execute a trust deed.

The Trustees protect the interest of the debenture holders through the powers granted by the trust deed.

B. Characteristics/Features of Debentures

A debenture is a written document or certificate which acknowledges the debt by the company.

The debenture certificate is issued under the common seal of the company.

Mode and period of payment of principal and interest is fixed and is stated in the debenture.

Rate of interest is fixed and is stated in the debenture.

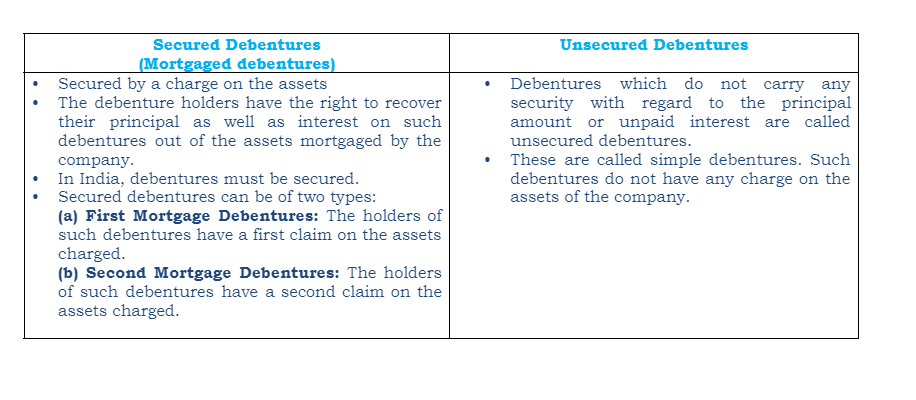

The debt taken by issue of debentures is usually secured by a charge on the assets of the company.

It is considered as an external equity or Long-term Borrowings of the company.

C. Distinction between Share and Debenture

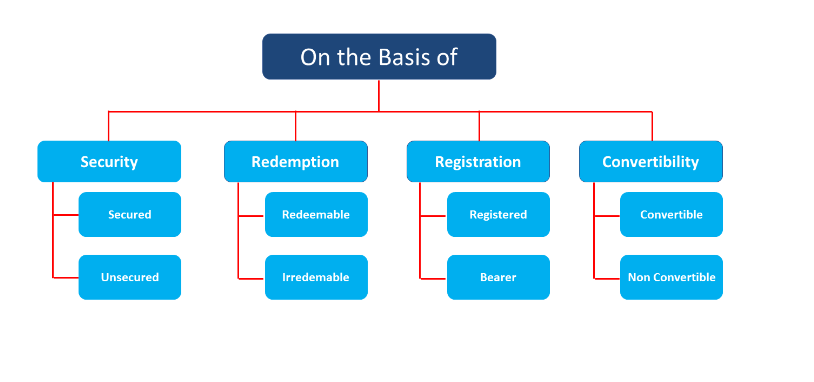

D. Type of Debentures

a) On the basis of Security

b) On the basis of Redemption

c) On the basis of Registration

d) On the basis of Convertibility

E. Disclosure in the Balance Sheet

Case-A Debentures are due for redemption after 12 months/operating cycle from the Balance Sheet date

Case-B Debentures are due for redemption within 12 months/operating cycle from the Balance Sheet date

F. Issue of Shares at Par, Premium or Discount

a) Par value

Par value means the nominal amount or face value of debenture

When issue price of the debenture is exactly equal to their nominal value or face value, Debentures are said to be issued at par

For example, debenture of face value of Rs. 100/- issued at Rs. 100/-

b) Premium

When the debentures of a company are issued at more than its nominal value (face value), the excess amount is called premium

The premium amount is credited to a separate account called ‘Securities Premium Account’ and is shown under the title ‘Equity and Liabilities’ of the company’s Balance Sheet under the head ‘Reserves and Surpluses’

For example, debenture of face value of Rs. 100/- issued at Rs. 120/- then it is said to be issued at premium of Rs. 20/-

c) Discount

When debentures are issued at less than their nominal value they are said to be issued at discount

For example, debenture of Rs. 100 each is issued at Rs. 90 per debenture

The discount is debited to a separate account called Discount on Issue of Debentures Account.

Discount on Issue of Debentures is written off in the same year in which debentures were allotted.

The write off is done from Capital Reserve, Securities Premium Reserve, General Reserve or from the Statement of Profit & Loss in that sequence.

The discount on issue of debentures is allowed on allotment.