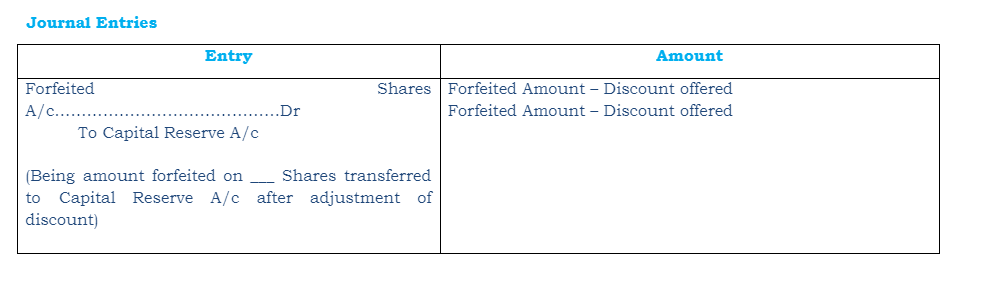

- If all the forfeited shares are reissued, the Forfeited Shares A/c will show a zero balance because whole of the amount in this account after adjusting the amount of discount allowed on reissue will be transferred to Capital Reserve account

- But in case, only a part of the forfeited shares are reissued and others remain cancelled, the amount forfeited on forfeited shares not reissued will remain in the Forfeited Shares Account

- Proportionate amount forfeited on share reissued will be calculated in the following manner: