The issue price of shares is payable in instalments i.e. on application, on allotment and on calls made from time to time by the Board of Directors of the Company.

Sometimes some shareholders fail to pay the called-up amount in full i.e., they do not pay one or more instalments after the allotment of the shares to them.

In such a case either the company can go to the court and file a suit against the defaulting shareholders for recovery of the due amount or can cancel the membership of the defaulting shareholders.

In case the membership is cancelled, the amount paid by the defaulting members towards share capital stands forfeited. It is called ‘Forfeiture of Shares.’

With the cancellation, the defaulting shareholder also loses the amount paid by him/her on such shares.

2) Effect and Results of the Forfeiture

Cancellation of membership of the defaulting shareholder.

Reduction of issued Share Capital of the company.

Company forfeits amount paid by Defaulting shareholder on such shares.

Defaulting shareholder loses amount paid by him/her on such shares.

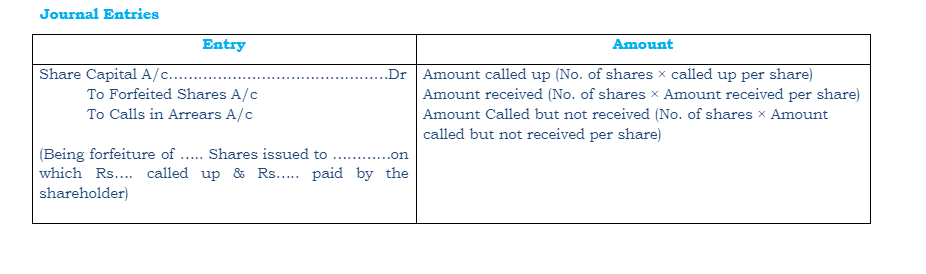

3) Accounting Treatment – Shares Issued at Par

4) Accounting Treatment – Shares Issued at Premium

Case -1 Premium on shares has been received prior to the forfeiture

Amount of Share premium once received, stays in the Securities Premium A/c and cannot be reversed or credited to any other account. Section 52 of the Companies Act, 2013 restricts usage of share premium for certain specific purposes only

In this case the journal entry of forfeiture of shares will be similar to the entry made as if the shares had been issued at par.

Case -2 Premium on shares has not been received prior to the forfeiture

In this case, amount of Share Premium is due but money against these are not yet received.

As the amount towards Share Premium will not be received, we will have to reverse the Securities Premium Reserve A/c as well as the Amount due