VI. SHARES ISSUED FOR CONSIDERATION OTHER THAN CASH, PRIVATE PLACEMENT AND EMPLOYEES STOCK OPTION PLAN (ESOP)

A. Accounting Treatment of Shares Issued for Consideration Other than Cash

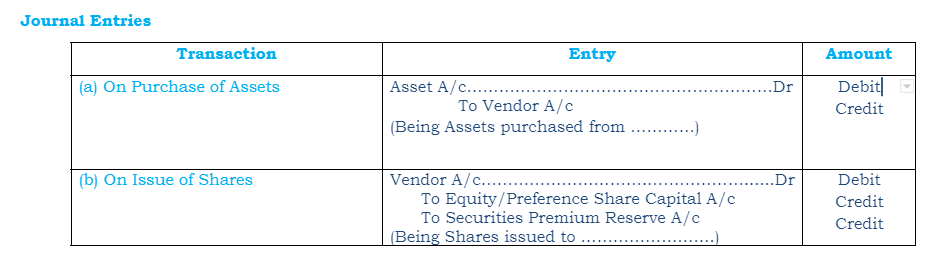

1) On Purchase of Assets

Where a company has purchased assets from a vendor and enters into an arrangement with the said vendor that instead of settlement of his dues in cash, the vendor agrees to accept fully paid shares of the company issued to them.

These shares can be issued at par or at premium, and the number of shares to be issued will depend upon the price at which the shares are issued and the amount payable to the vendor

The number of shares issued to the vendor will be calculated as = Amount Payable/ Issue Price

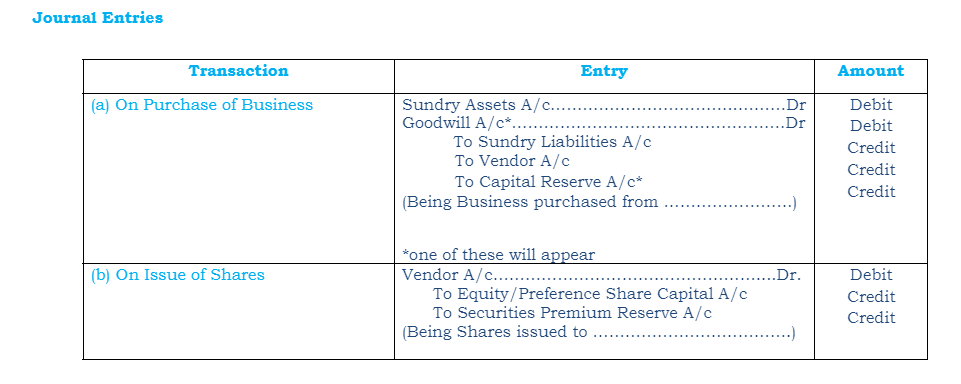

2) On Purchase of Business

Where a company purchases business of another entity and enters into an arrangement with the said entity that instead of settlement of their dues in cash, the owners of the entity agrees to accept fully paid shares of the company issued to them.

These shares can be issued at par or at premium, and the number of shares to be issued will be calculated as Purchase Consideration Amount/Issue price

3) Issue of Shares to Promoters

Sometimes shares are issued to the promotors of the company in lieu of the services provided by them during the incorporation of the company.

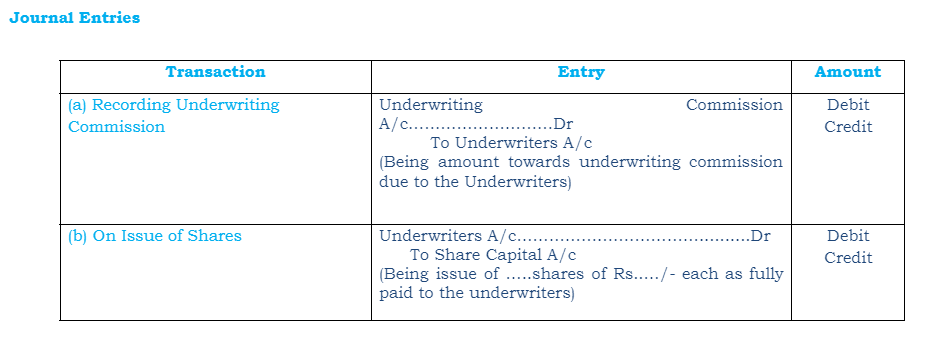

4) Issue of Shares to Underwriters

The Company enters a contract with a person know an Underwriter who takes the shares in his own name which are not subscribed by the public. The Underwriter charges a commission for his servicers.

Important:-

Issue of shares for consideration other than cash are disclosed separately under disclosure of “Share Capital” in the notes to the accounts as subscribed and fully paid-up capital

B. Private Placement of Shares

Definition & Meaning

Private Placement as per Section 42 means:

any offer or invitation to subscribe or issue of securities

to a select group of persons by a company (other than by way of public offer)

through private placement offer-cum-application, which satisfies the conditions specified in this section.

Features

There are three features which distinguish the private placement from other issues.

Securities to be issued to the selected group of person

It should not be a public issue.

Issued as per the provision of this section i.e. Section 42.

Offer/ Invitation to subscribe for shares

Maximum 50 persons in one go

200 persons in aggregate in one financial year

These limits are individually applicable for each kind of securities

Minimum Investment value

Investment size of not less than INR 20,000/- of face value of securities per person

C. Employees Stock Option Plan

Meaning

Employee stock option plan (ESOP) or Equity incentive plan is the scheme used by the companies to give ownership interest to its employees. ESOP is regulated by Section 62(1) (b) of the Companies Act, 2013

An ESOP is an option given to its whole time directors and permanent employees the benefit or the right to purchase the stock of the company at a predetermined price which is generally at lower than market price. The participation in this scheme by the employees is purely voluntary.

Shares allotted under this scheme are locked for a minimum period of one year from the allotment date

Procedure followed for the formulation of ESOPs

A Compensation committee is formulated by the Board of Directors and consist of a majority of independent directors

The Compensation Committee drafts a plan in accordance with the guidelines provided by the SEBI

The Compensation Committee presents the ESOP to the Board of Directors and seeks their approval

The plan is approved by majority shareholders (3/4th of the total shareholders) through a special resolution.

Management / Compensation committee decides on list of employees to whom ESOPs are to be granted & places it before Board for approval through ordinary resolution. This is again ratified by Shareholders at meeting held at future dates.

After approval from Board of Directors, Management issues letter of acceptance to employees. After receipt of letter of acceptance of option, employees are eligible to exercise options once these are vested as per ESOP plan.

The Company holds a Board Meeting at regular intervals during the exercise period for allotment of shares on options exercised by the employees.