In general, shares are issued for cash. The company may call the share money either in one instalment or in two or more instalments. But company always collects this money through its bankers.

A. Receipt of Share Money in One Instalment

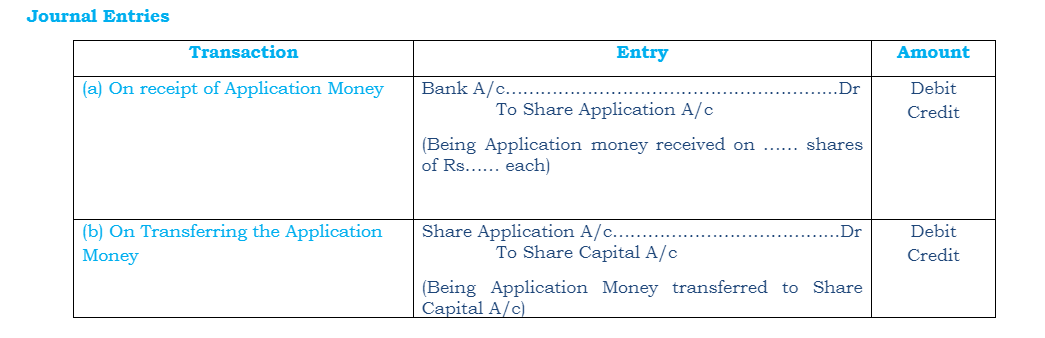

The company may receive the share money in one instalment along with application. In this case the following journal entries are made in the books of the company

B. Receipt of Share Money in Two or More Instalments

Instead of receiving payment in one instalment i.e. at the time of application the company collects it in two or more instalments.

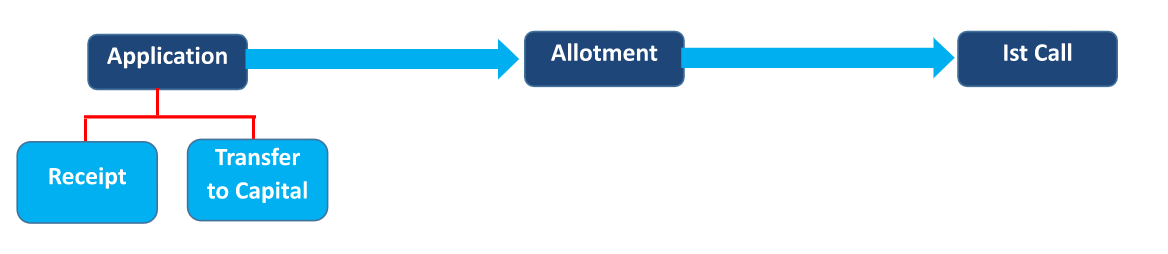

The first, instalment which the applicants have to pay along with the applications for shares is known as Application Money.

On the allotment of shares the allottees are required to pay the second instalment which is termed as Allotment Money.

If the company decides to call the share money in more than two instalments the other instalment is/are termed as Call Money (i.e. first-call, second call or final call).

a) Receipt of Share Application Money

b) Allotment Money becoming due:

On the allotment of shares the amount receivable on the next instalment i.e. on allotment becomes due.

c) Call on Shares

After the receipt of application and allotment money the money that remains unpaid can be called up by the company as and when required

Thus a call is a demand made by the company asking the shareholders to remit the called up amount on shares allotted to them.

The company may demand the remaining money in more than two instalments. The amount called after the allotment is known as call money. There may be one or more calls, depending on the fund requirements of the company.

If the company makes more than one call the same accounting treatment is followed for recording the second call or third call money due and their receipt. The last call made is termed as final call.

2. Issue of Shares at Par or Premium

a) Par Value

Par value means the nominal amount or face value of share

When issue price of the share is exactly equal to their nominal value or face value shares are said to be issued at par

For example, share of face value of Rs. 10/- issued at Rs. 10/-

b) Premium

When the shares of a company are issued at more than its nominal value (face value), the excess amount is called premium

The premium amount is credited to a separate account called ‘Securities Premium Account’ and is shown under the title ‘Equity and Liabilities’ of the company’s balance sheet under the head ‘Reserves and Surpluses’

For example, share of face value of Rs. 10/- issued at Rs. 12/- then it is said to be issued at premium of Rs. 2/-

c) Securities Premium Reserve

As per Section 52(1) of the Companies Act, 2013, where company issues shares at a premium, whether for cash or otherwise, a sum equal to aggregate amount of premium received in those shares shall be transferred to separate account called Securities Premium Account.

As per Section 52(2) of the Companies Act, 2013 Securities Premium Amount may be applied or utilized for the following purposes

To write off preliminary expenses of the company

To write off the commission paid or discount/expenses on issue of shares/debentures.

To issue fully paid-up bonus shares to the existing shareholders.

To provide premium on the redemption of preference shares or debentures of the company.

To buy back of its own shares as per Section 68: The term buy back of shares implies the act of purchasing its own shares from stock market by a company either from free reserves, securities premium reserve or proceeds of any shares or debentures.