Partnership - Retirement

Topic - 1 | RETIREMENT - MEANING & BASIC CONCEPTS:

Study Material & Notes

Study Material & Notes for the Chapter 6

Partnership – Retirement of Partner

I. RETIREMENT – MEANING AND BASIC CONCEPTS

A. Meaning of Retirement of a Partner

When one or more partners leave the firm and the remaining partners continue to do the business of the firm is called Retirement of a Partner. Retirement of a partner means that the partner ceases to be a partner of the firm. It results in reconstitution of the firm by which old partnership comes to an end and a new partnership among the continuing (remaining) partners comes into existence.

B. Effect

Due to retirement, the existing partnership comes to an end and the remaining partners form a new agreement and the partnership firm is reconstituted with new terms and conditions. At the time of retirement the retiring partner’s claim is settled.

C. Different ways a Partner may retire:

- With the consent of all partners (If all other partners agree to this retirement)

- As per the terms of the agreement (If there is an agreement to that effect…say partner will retire on 31-Mar-2022). The terms and conditions of retirement of a partner are normally provided in the partnership deed. If not, they are agreed upon by the partners at the time of retirement.

- At his/her own will i.e. If he/she has given his/her consent in writing to retire

D. Liability of the Retiring Partner – for the acts before Retirement Section 32(2)

- A retiring partner remains liable for all the acts of the firm up to the date of his retirement.

- However, a retiring partner may be discharged from his liability by an agreement between himself, third party and the continuing partners

E. Liability of the Retiring Partner – for the acts after Retirement Section 32(3)

- A retiring partner also continues to be liable to third parties for the acts of the firm even after his retirement until a public notice of his retirement is given.

- A public notice is served either by way of a notification in the Official Gazette or published in a English & Hindi Newspaper

F. Accounting issues at the time of Retirement

- Determination of New Profit Sharing Ratio and Gaining Ratio

- Adjustment for Goodwill

- Treatment of Reserves & Losses

- Revaluation of assets and liabilities

- Settlement of retiring partner’s dues

- New Capital of the Continuing partners

Topic - 2 | DETERMINATION OF NEW PROFIT SHARING RATIO & GAINING RATIO:

Study Material & Notes

Study Material & Notes for the Chapter 6

Partnership – Retirement of Partner

II. DETERMINATION OF NEW PROFIT-SHARING RATIO & GAINING RATIO

A. Change in Profit-Sharing Ratio

Change in the Profit-sharing ratio is required as the partner who retires surrenders his/her share in favour of the continuing/remaining partners.

B. New Profit-Sharing Ratio

New Profit-Sharing ratio is the ratio in which the continuing/remaining partners decides to the share the profits of the firm in future. It is decided as per the mutual agreement amongst the continuing/remaining partners.

C. Gaining Ratio

At the time of retirement of an existing partner, the remaining or continuing partners acquire the share of profits from the retiring or outgoing partner. The ratio in which remaining partners acquire retiring partner’s profit share is known as gaining ratio.

D. Purpose of Gaining Ratio computation

Gaining ratio is required because the remaining partners will pay the retiring partner’s share of goodwill in their gaining ratio.

E. Gaining/Sacrificing Share

Gaining /(Sacrificing) Share = New Share – Old Share

- If a Partner’s New Share – Old Share is Positive(+) figure then the partner has made a gain

- If a Partner’s New Share – Old Share is Negative(-) figure then the partner has made a sacrifice

F. New Profit Sharing ratio and Gaining/Sacrificing Share

Case-1 Retiring Partner’s Share Distributed in Existing Ratio – Silent on new ratio

- In this case, retiring partner’s share is distributed in existing ratio amongst the remaining partners.

- The remaining partners continue to share profits and losses in the existing

- Gaining Ratio is the existing ratio amongst the remaining partners

Important to Note:

- In absence of any information in the question, it will be presumed that retiring partner’s share has been distributed among the remaining partners in existing (old) ratio

Case-2 Retiring partner’s share distributed in Specified proportion – OF Case

- Sometimes the remaining partners purchase the share of the retiring partner in specified ratio.

- The share purchased by them is added to their old share and the new ratio is arrived at.

- Gaining Ratio is the specified share acquired from the Retiring partner

Case-3 Retiring partner’s share is taken by one of the Partners

- The retiring partner’s share is taken up by one of the remaining partners.

- In this case, the retiring partner’s share is added to that of existing partner’s share. Only his/her share changes.

- The other partners continue to share profit in the existing ratio.

- Gaining Ratio – One partner acquires full share of the Retiring partner

G. Distinction between sacrificing ratio and gaining ratio?

Topic - 3 | VALUATION & ADJUSTMENT OF GOODWILL:

Study Material & Notes

Study Material & Notes for the Chapter 6

Partnership – Retirement of Partner

III. VALUATION AND ADJUSTMENT OF GOODWILL

A. Accounting Treatment of Goodwill

- The retiring partner is entitled to his/her share of goodwill at the time of retirement because the goodwill of the firm has been earned with the efforts of all the existing partners including the retiring partner.

- Hence, at the time of retirement of a partner, goodwill is valued as per agreement among the partners.

- The retiring partner is compensated for his/her share of goodwill by the continuing partners (who have gained due to acquisition of share of profit from the retiring/deceased partner) in their gaining ratio.

- The accounting treatment for goodwill in such a situation depends upon whether or, not goodwill already appears in the books of the firm.

- Therefore, in case of retirement of a partner, the goodwill is adjusted through partner’s capital accounts. The retiring partner’s capital account is credited with. his/her share of goodwill and remaining partner’s capital account is debited in their gaining ratio.

B. When Goodwill is already appearing in the books

- As per Accounting Standard-26 (AS-26), goodwill can be recorded/debited in the books only when some consideration in money or money’s worth has been paid for it.

- Thus only purchased goodwill should be recorded in the firm’s books

- If at the time of retirement of a partner, goodwill is appearing in the Balance sheet of a firm, it would be desirable to close the Goodwill Account

C. Goodwill is not appearing in books and computed-Known Goodwill

Step-1 Firm’s Goodwill = Its given in the question or computed as per valuation methods

Step-2 Goodwill Share of the Retiring Partner = Firm’s Goodwill X Retiring Partner’s share

Step-3 Goodwill Share of the Remaining Partner = Goodwill share of the Retiring Partner X Gaining Ratio

The goodwill is adjusted through partner’s capital accounts. The retiring partner’s capital account is credited with. his/her share of goodwill and remaining partner’s capital account is debited in their gaining ratio.

D. Hidden Goodwill

If the firm has agreed to settle the retiring or deceased partner’s account by paying him a lump sum amount, then the amount paid to him in excess of what is due to him, based on the balance in his capital account after making necessary adjustments in respect of accumulated profits and losses and revaluation of assets and liabilities, etc., shall be treated as his share of goodwill (known as hidden goodwill).

Hidden Goodwill = Total Lumpsum payment to the Retiring partner – Retiring Partner’s adjusted capital balance

Topic - 4 | RESERVES, ACCUMULATED LOSSES & REVALUATION:

Study Material & Notes

Study Material & Notes for the Chapter 6

Partnership – Retirement of Partner

IV. ACCOUNTING TREATMENT OF RESERVES, ACCUMULATED PROFITS, REVALUATION

- On retirement of a partner, the partners scans Firm’s Financial position (Balance Sheet) i.e. Reserves, Accumulated Losses, Assets & Liabilities.

- As learnt in case of Admission of partner, this is done to ensure no partner(s) get(s) undue benefit due to previously earned/unearned profits or suffer loss due to previous earned/unearned losses.

- Free Reserves like General Reserve, P&L (Cr), these are distributed among partners in their existing profit-sharing ratio.

- Specific purpose reserves like (a) Workmen Compensation Reserve are compared with any workmen claim (b) Investment Fluctuation Reserve is compared with market value of Investments and any excess reserve is distributed to existing partners in their current PSR and any short reserve is taken to Revaluation A/c.

- Any Undistributed Losses or Fictitious Assets are written off and charged to the existing Partners in their current Profit Sharing Ratio.

- Partners reevaluate market value of Fixed Assets and remeasure Current Assets and Current Liabilities. Any change in the value of Assets/Liabilities is dealt via Revaluation Account and the resultant gain/loss is shared amongst the existing partners in their current profit-sharing ratio.

Topic - 5 | ACOMPUTATION & METHOD OF PAYMENT TO RETIRING PARTNER:

Study Material & Notes

Study Material & Notes for the Chapter 6

Partnership – Retirement of Partner

V. PAYMENT TO RETIRING PARTNER

A. Computation of Amount Due to the Retiring Partner

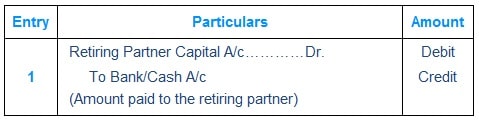

B. Settlement of Retiring Partner’s Claim – In Lumpsum

Retiring partners’ claim is paid either out of the funds available with the firm or out of funds brought in by the remaining partners.

Journal Entry

C. Settlement of Retiring Partner’s Claim – In Installments

- Amount due to retiring partner is paid in instalments. Usually, some amount is paid immediately on retirement and the balance is transferred to his loan account.

- This loan is paid in one or more instalments and the loan amount carries some interest.

- In the absence of any agreement on interest rate, the retiring partner can claim interest @ 6% [as per Section 37 of the Indian Partnership Act 1932]

- Installment has two parts – Principal Amount of Loan and Interest at agreed rates

- Interest due on loan amount is credited to retiring partners’ loan account.

- Instalment inclusive of interest then is paid to the retiring partner as per schedule agreed upon.

Journal Entry

D. Mid Term Retirement

- Mid term retirement categorize the adjustments in two parts

- From previous balance sheet date

- Examples: Goodwill, Reserves, Undistributed Profits/Losses Misc. Expenditure on Assets side, revaluation Profit/Loss etc.

- There is no change in these values if partner retires mid term

- Period specific adjustments

- Examples: like Salary, Drawings, Interest on Capital, Interest on Drawings, share of current account year profit/loss.

- In such adjustments, time factor is used.

- The Estimated Profit/Loss till the date of retirement is credited/debited to the Retiring partner A/c

- From previous balance sheet date

- Mid Term Retirement-Interest payment to Retiring Partner

-

- Interest is accrued on (i) End of the Financial year and (ii) Date of Payment

- Installment is paid on date of payment along with interest

-

Topic - 6 | ADJUSTMENT OF CAPITALS:

Study Material & Notes

Study Material & Notes for the Chapter 6

Partnership – Retirement of Partner

VI. ADJUSTMENT OF CAPITAL

- Sometime, at the time of retirement, the remaining partners’ agree that their capitals be adjusted

- To begin with, New Capital of the reconstituted Firm is determined

- The partners may decide to keep the New Capital at the same level as it was there in the business before retirement of partner or decide a lump-sum figure

- New Capital can be equal to combined adjusted closing capital of remaining partners or with addition towards shortage of the amount payable to retiring partner + desired cash balance to be maintained in business

- For this purpose, the capital accounts of the existing partners are prepared, making all adjustments, on account of goodwill, free reserves , accumulated losses and revaluation of assets/reassessment of liabilities.

- The actual capital so adjusted will be compared with the amount of capital that should be kept in the business after the admission of the new partner.

- The excess if any, of adjusted actual capital over the proportionate capital will either be withdrawn or transferred to current account and vice versa.

Methods of Capital Adjustment

I. When Total Capital of the New Firm is Given

Step-1 Firm’s Total Capital = Given in the Question already

Step-2 Specific Partner’s New Capital

= Firm’s Total New Capital (as per Step-1) X Specific Partner’s Share per new PSR

Step-3 Specific Partner’s Existing Adjusted Closing Capital

= Old Capital +(-) Adjustments of Goodwill, Reserves & Accumulated losses

Step-4 Capital to be introduced/ withdrawn

= Specific Partner’s New Capital – Specific Partner’s Existing Adjusted Closing Capital

II. When Total Capital of the Remaining Partners is to be in their New Profit-Sharing Ratio

Step-1 Firm’s Total Capital = Combined Adjusted Closing Capital of remaining partners

Step-2 Specific Partner’s New Capital

= Firm’s Total New Capital (as per Step-1) X Specific Partner’s Share per new PSR

Step-3 Specific Partner’s Existing Adjusted Closing Capital

= Old Capital +(-) Adjustments of Goodwill, Reserves & Accumulated losses

Step-4 Capital to be introduced/ withdrawn

= Specific Partner’s New Capital – Specific Partner’s Existing Adjusted Closing Capital

III. When Total Capital of New Firm is equal to Total Capital before retirement of a partner

Step-1 Firm’s Total Capital = Total Capital of all the Partners including retiring partner before adjustments (as per Balance Sheet given)

Step-2 Specific Partner’s New Capital

= Firm’s Total New Capital (as per Step-1) X Specific Partner’s Share per new PSR

Step-3 Specific Partner’s Existing Adjusted Closing Capital

= Old Capital +(-) Adjustments of Goodwill, Reserves & Accumulated losses

Step-4 Capital to be introduced/ withdrawn

= Specific Partner’s New Capital – Specific Partner’s Existing Adjusted Closing Capital

IV. When the Retiring Partner is paid through amount brought by the remaining partners in a manner to make their capitals proportionate to their New Profit-sharing Ratio

Step-1 Firm’s Total Capital = Combined adjusted closing capital + Shortage of the amount to be paid to retiring partner

Step-2 Specific Partner’s New Capital

= Firm’s Total New Capital (as per Step-1) X Specific Partner’s Share per new PSR

Step-3 Specific Partner’s Existing Adjusted Closing Capital

= Old Capital +(-) Adjustments of Goodwill, Reserves & Accumulated losses

Step-4 Capital to be introduced/ withdrawn

= Specific Partner’s New Capital – Specific Partner’s Existing Adjusted Closing Capital

V. When the Retiring Partner is to be paid through amount brought by the Remaining partners in a manner to make their Capitals proportionate to their New Profit-sharing Ratio and also leave a desired Cash Balance

Step-1 Firm’s Total Capital = Combined adjusted closing capital + Shortage of the amount to be paid to retiring partner + Desired Cash balance

Step-2 Specific Partner’s New Capital

= Firm’s Total New Capital (as per Step-1) X Specific Partner’s Share per new PSR

Step-3 Specific Partner’s Existing Adjusted Closing Capital

= Old Capital +(-) Adjustments of Goodwill, Reserves & Accumulated losses

Step-4 Capital to be introduced/ withdrawn

= Specific Partner’s New Capital – Specific Partner’s Existing Adjusted Closing Capital

Journal Entries

a. When excess amount is withdrawn by the partner or transferred to current

a. When excess amount is withdrawn by the partner or transferred to current